Medi-Share Overview: My household’s expertise this yr

Final yr, I wrote a evaluation of Medi-Share from my perspective as an insurance coverage skilled. This yr, I need to share my expertise as a Medi-Share member.

With main medical premiums rising and physician networks shrinking, I discovered myself in the identical state of affairs as a lot of my purchasers: how do I afford this and hold my household lined? Medi-Share appeared a pretty possibility: decrease premiums, a PPO physician community that my spouse’s OBGYN and youngsters’ pediatrician was on, a very tacky web site (it is gotten a little bit higher), and decrease premiums (did I say that already?).

However how wouldn’t it truly work? We have been anticipating some main modifications too–my spouse was pregnant and we have been anticipating child boy #3 through the summer season. Would this actually be possibility for us?

For those who’re on the lookout for a fast abstract, right here it’s: Medi-Share is a implausible possibility however there’s a little bit little bit of a studying curve concerned.

When you get the cling of it although, I feel most people and households shall be happy. You’ll be able to soar proper into our web site to check Medi-Share to different plans in your space, or proceed studying to get the main points.

Issues to know earlier than you join Medi-Share

Medi-Share doesn’t exclude folks for pre-existing situations (just like main medical plans), however they will not pay for any pre-existing situations for the primary 36 months. Essential!

For our household, this meant my spouse was not candidate since she was already pregnant once we have been signing up. We determined to depart her on the key medical plan we had earlier than (Aetna) and transfer me and the then 2-year-old twin boys onto Medi-Share. My spouse and new child would transfer over with us after the child was born (extra on that call later).

Signing up was straightforward, however a little bit completely different than the opposite insurance coverage corporations (do not forget that studying curve factor I discussed?). When you apply to Medi-Share, you are not mechanically enrolled. There are just a few extra varieties and signatures that you must full about your medical historical past in addition to signal a press release of religion and supply some church references. Nobody ever checked our references however now we have had purchasers inform us that their’s have been.

You additionally must arrange your sharing account with the financial institution. There is a small charge and a few paperwork concerned, however general fairly painless. There isn’t any Open Enrollment requirement for Medi-Share that means you may join anytime, however they advocate you submit your preliminary software by the twentieth of the month in order for you your plan to begin the first of the following month. Is smart primarily based on our experience–it took a couple of week.

The PPO physician community is legit

One of many causes we selected Medi-Share personally and determined to characteristic it on our web site is that they have a legit PPO physician community. Lots of the different sharing ministries allow you to see any physician you need, however the benefit of being “in-network” with a PPO is you get negotiated reductions. It is a nice start line versus having to haggle over money costs (typically higher, typically a lot worse)

More often than not, your physician’s front-office employees won’t have heard of “the Medi-Share community”, so do not panic in case you ask they usually have a look at you humorous. Medi-Share makes use of the “Multiplan PHCS community”. They will possible nod their head in case you ask about that.

We have added Medi-Share’s physician community to our physician search characteristic at in our insurance coverage information at TakeCommandHealth.com, so it will be straightforward so that you can see in case your physician’s are “in community” or not. You’ll be able to nonetheless see docs “out of community” and Medi-Share pays, however they will solely cowl what the negotiated fee would have been and also you’re by yourself for the remaining. Sounds fairly honest to me. (Observe: For those who see go to an out-of-network hospital, there is a $500 charge along with any quantities over the negotiated fee, except it is an emergency)

Medi-Share handles payments in another way

The largest distinction with Medi-Share was determining how billing works. It was a little bit complicated at first, however after you get the cling of it, I feel it is truly a lot extra easy than different main medical plans.

With Medi-Share, there are not any deductibles or max-out-of-pocket limits, simply this factor referred to as an Annual Family Portion (AHP) that’s type of like a deductible and max-out-of-pocket restrict rolled collectively. In actual easy terms–you pay all the things earlier than your AHP, after which nothing after your AHP (for eligible companies, extra on that in a second).

Medi-Share additionally does not have co-pays for physician visits, they’ve a $35 “supplier charge”. You pay this charge everytime you see a physician (major care or specialist). It doesn’t rely in the direction of your AHP however does go in the direction of your physician invoice. Most individuals won’t ever know the distinction, however as an insurance coverage insider, right here it’s: Say your physician prices a $100 charge for a 15 minute session. In case your plan has a $35 copay, you’ll simply pay $35 and your insurance coverage would pay the remaining. With Medi-Share, you pay the $35 supplier charge after which get a invoice later for the remaining $65 (which does go in the direction of your AHP). Not a enormous deal as most individuals will in all probability by no means discover, however one thing to level out.

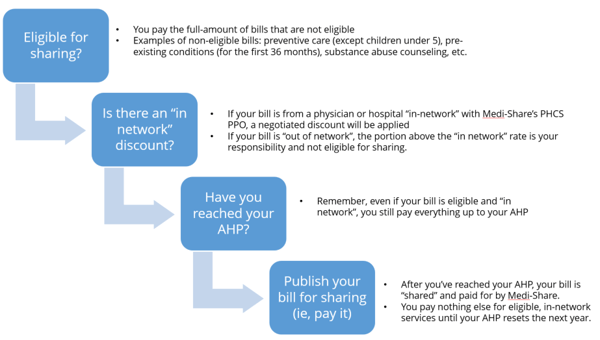

Here is a helpful graphic that explains how Medi-Share billing works:

Here is a fast instance operating by means of the steps above. For example you are on the AHP 2500 plan and get sick and spend an evening within the hospital:

- Is the invoice “eligible for sharing” –> Sure

- Is there an “in community” low cost? –> Assuming you went to a hospital in Medi-Share’s community, you’ll get the negotiated charges. For example the price of your hospital keep is $8,000, however the negotiated fee is $6,000. The hospital will ship your invoice to Medi-Share they usually’ll apply the right charges for you.

- Have you ever reached your AHP? –> If that is the primary invoice you have got, then no, you have not. For those who’re on the AHP 2500 plan, you pay $2,500, after which the remaining $3,500 is revealed for sharing. Another eligible payments you or anybody in your loved ones have that yr are lined since you have met your AHP.

In abstract, your $8,000 hospital invoice prices you $2,500 out-of-pocket. Not dangerous! And rather more easy than attempting to determine your deductible, coinsurance, and copays on an everyday medical plan.

Preventive care just isn’t actually lined

My spouse and I welcomed child boy #3 this July. I discussed I left my spouse on our previous Aetna plan whereas she had the child since we weren’t enrolled in Medi-Share earlier than the being pregnant and thus it might have been excluded from protection above (would have failed query #1). That was transfer. I then moved my spouse and new child over to Medi-Share to economize (they Aetna premiums have been loopy excessive). That was a medium-good transfer. I am going to clarify.

I had learn within the Medi-Share pointers that preventive care was “eligible for sharing” for newborns and youngsters as much as 5 years previous. This was good as a result of our new child was about to have all of his new child check-ups and immunizations, all issues which might be thought-about preventive and lined for $0 with a serious medical plan.

Not so with Medi-Share. I acquired a invoice for almost $1,000 for my child’s immunizations! Going again to the chart above, simply because preventive care for teenagers as much as 5 years previous is “eligible for sharing”, doesn’t suggest it will not price me one thing. It was eligible for sharing (passes step 1), the in-network low cost was utilized (step 2), however I had not reached my household’s AHP but (step 3) so I acquired a invoice for the immunizations.

It is smart on reflection, however was a little bit sudden. As a facet be aware, I submitted the invoice to our new negotiation service with Take Command Well being–they referred to as the pediatricians workplace and labored with Medi-Share to get just a few hundred {dollars} knocked off for me. Not dangerous! I’ve additionally since discovered that you could get immunizations for youngsters fairly low cost on the county hospital–I’ve had some extra expertise Medi-Share mother and father advocate paying for the physician go to together with your pediatrician after which go to the county for immunizations.

At first, I used to be kicking myself for not leaving my new son on the previous Aetna plan for an additional month or two the place his new child checkups and immunizations would have been $0. Nonetheless, Medi-Share units their premium charges for singles, {couples}, after which households of three or extra. With 5 folks on our Medi-Share plan, I wasn’t going to save lots of any cash by leaving one child and even my spouse and child on Aenta. So lengthy story brief, I nonetheless got here out manner forward with the cheaper premiums on Medi-Share however was caught off guard a little bit bit by the immunization invoice.

Customer support and add-ons

Medi-Share’s customer support has been nice. They typically pray for you if you name too. At first I assumed it was unusual over the cellphone, however the account managers actually know their stuff and sustain with you and your loved ones. We’ve not crossed our AHP but to have our payments shared, however we frequently get postcards to wish or write notes for different households which have. They do not disclose why (that will be a privateness violation) nevertheless it’s nonetheless fairly cool.

Medi-Share lately added some primary ancillary merchandise together with telemedicine with MDLive and a dental low cost program with Carrington. These are mechanically included in your month-to-month share quantity. Telemedicine is a brilliant transfer as a result of as a substitute of paying the $35 supplier charge, you may name and get primary prescriptions over the cellphone for $0.

Nonetheless, I am actually glad I used Take Command’s Premier membership plan together with Medi-Share. Though our telemedicine supplier Teladoc and MDLive are admittedly a little bit redundant, Take Command’s dental community with Aetna was a lot bigger and had our dentist whereas the Carrington community didn’t. Additionally, the invoice negotiation service paid for itself with the cash it saved me on the primary invoice.

Full Disclosure: Sure, we made a small margin if you join Take Command’s Premier membership plan, however I discovered it to be price it and a pleasant complement as a Medi-Share member.

Conclusion and subsequent steps

We’ll be persevering with with Medi-Share this subsequent yr and would extremely advocate it! As I discussed, there’s a little little bit of a studying curve and I am actually grateful I had our invoice negotiation service at my disposal to assist. Though the immunization invoice caught me unexpectedly, now that I perceive Medi-Share’s billing course of a little bit higher issues like that will not shock me. Once you consider what we’re saving on premiums every month, we nonetheless come out manner forward on Medi-Share than we might with a serious medical plan.

If Medi-Share is constant together with your values and religion, I feel it is price a critical look. For those who’re eligible for a tax-credit or have a pricey pre-existing situation, I might ensure that to weigh your different choices earlier than signing up.

One of the best factor to do? See how Medi-Share compares to different main medical plans in your space by going by means of our self-guided interview at TakeCommandHealth.com. So far as we all know, we’re the one web site that permit’s you evaluate Medi-Share side-by-side with Market and off-exchange main medical plans in your space. Use our free web site to rapidly seek for your docs and prescriptions and simulate your situations to see if Medi-Share can be match for you and your loved ones.

And naturally, when you have any questions, be at liberty to ask within the feedback beneath or e mail me at assist@takecommandhealth.com and I might be comfortable to reply your questions!

Observe: Medi-Share doesn’t pay commissions like typical medical plans, however we do make a small advertising and marketing charge when customers join by means of our web site. It retains us in enterprise and doesn’t price you a penny.

About Take Command Well being

Take Command Well being launched three years in the past with the aim of bringing consciousness, advocacy, and transparency to the complicated world of medical insurance for small companies and people. Take Command Well being is on the forefront of this difficulty, a acknowledged chief in QSEHRA administration, ICHRA administration, small enterprise medical insurance and small enterprise HRA tax technique, with prospects in each state. It operates in Arizona, California, Florida, Georgia, Indiana, Michigan, North Carolina, Pennsylvania, Texas, Tennessee, and Wisconsin for particular person insurance coverage and provides small enterprise HRA administration nationwide.

Particular person

Jack

I wrote this weblog to assist folks make sensible medical insurance choices. I’m a small enterprise proprietor, a husband, and a dad to 3 boys, so I’ve seen firsthand how vital understanding insurance coverage choices will be. As a co-founder of Take Command Well being and a licensed well being skilled, I have been acknowledged as a number one skilled on healthcare transparency and outlined contribution preparations (QSEHRA). I have been featured within the New York Occasions, Wall Avenue Journal, Dallas Morning Information, Forbes and others. Be taught extra about me and join with me on our about us web page. Thanks!

Take Command is a Dallas-based tech startup on a mission to enhance the healthcare system, beginning with medical insurance. Self-described HRA nerds, we assist employers reimburse staff for particular person medical insurance utilizing HRAs.

Up Subsequent

Particular person

ICHRA for the self employed – the way it works

Keely S. • March 25, 2022